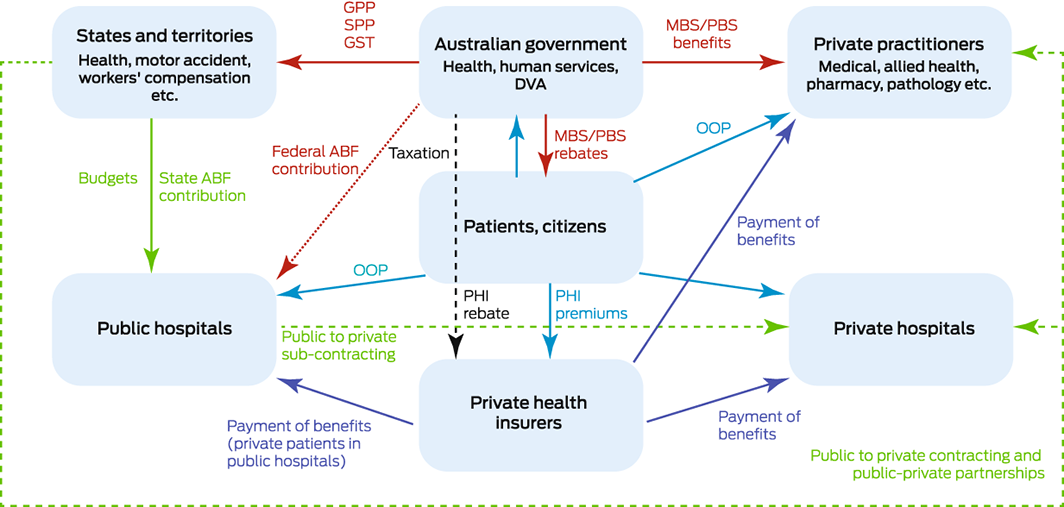

In 2021, the overall performance of the Australian health care system was ranked third of eleven high income countries by the Commonwealth Fund (New York), but only eighth for providing affordable, timely access to care.1 As in other countries, the Australian health care system has been challenged by coronavirus disease 2019 (COVID‐19), leading to the establishment of a major taskforce for improving access to primary health care.2 The publicly funded universal health care scheme introduced in 1984, Medicare, is underpinned by principles of simple, fair, and affordable health care.3 But Medicare is a complex system comprising multiple financial schemes at the federal and state levels and subsidies to the private sector (Box 1).

In this review, we identify the financing and policy challenges for Medicare and universal health care in Australia, as well as opportunities for whole‐of‐system strengthening. In particular: What have been the major challenges and problems for the Australian universal health care system since 2000? What policy reforms have been proposed to improve the system?

Methods

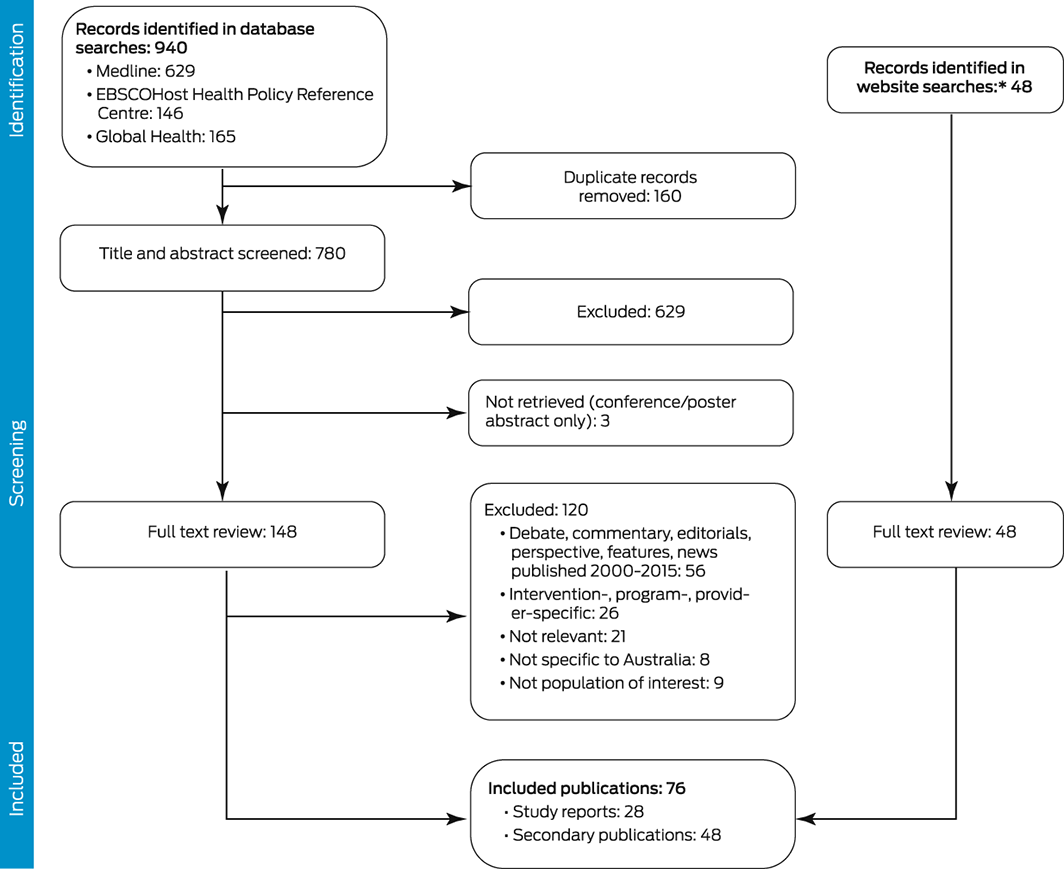

We searched the MEDLINE Complete, Health Policy Reference Centre, and Global Health databases (all via EBSCO) for publications to 14 August 2021 on Medicare, the Pharmaceutical Benefits Scheme, and the universal health care system in Australia. For further studies and grey literature we searched the Analysis & Policy Observatory (APO; https://apo.org.au), the Australian Indigenous HealthInfoNet (https://healthinfonet.ecu.edu.au), the Australian Public Affairs Information Service (APAIS; https://search.informit.org/ourcollections/indexes/APAIS), Google, Google Scholar, and the Organisation for Economic Co‐operation and Development (OECD) websites (https://data.oecd.org/healthres/health‐spending.htm). The major search term concepts were “Medicare”, “Pharmaceutical Benefits Scheme”, “health financing”, “out‐of‐pocket costs”, “universal healthcare”, and “public–private sector partnership” (Supporting Information, part 1).

Study selection, data extraction

For this review, we included articles on the Australian health care system published since 2000 that reported quantitative or qualitative research or data analyses; we also included opinion articles, debates, commentaries, editorials, perspectives, and news reports published from 1 January 2015. We excluded articles in languages other than English, program‐, intervention‐ or provider‐specific articles, publications regarding groups not fully covered by Medicare (eg, asylum seekers, prisoners), and search results for which full text was not available (eg, conference abstracts).

Author MA screened the titles and abstracts of retrieved items for relevance; authors MA, PC, and MH independently reviewed the full text of articles for eligibility. The included articles were grouped by emergent themes for our analysis.

Results

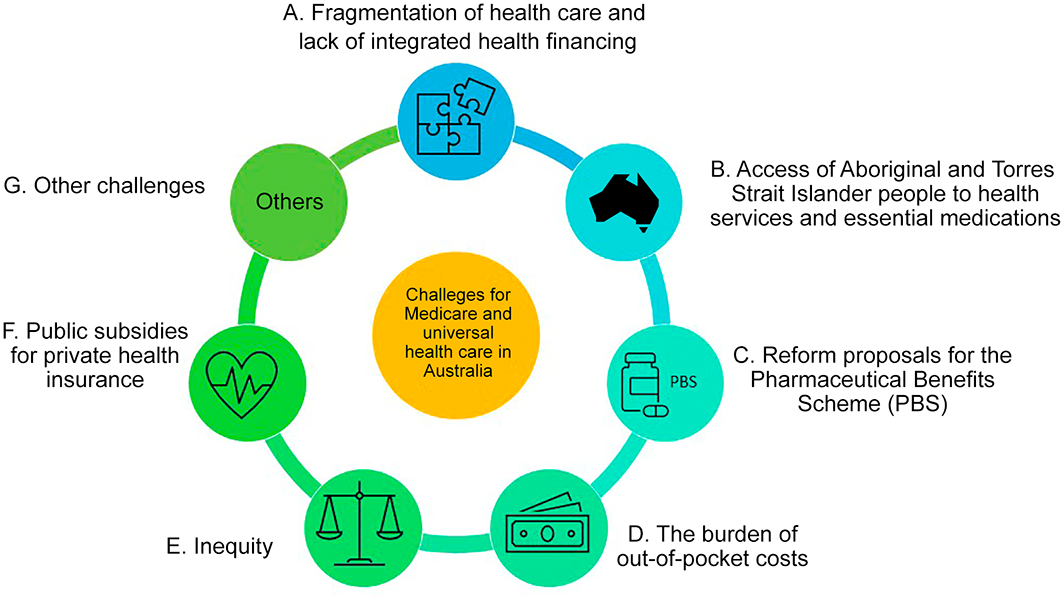

Our database search identified 940 potentially relevant publications; after screening and full text review, 28 study reports were deemed eligible for our review. A further 48 items identified by website searches were also included (Box 2; Supporting Information, part 2). We identified seven major themes in the included articles (Box 3).

Fragmentation of health care and the lack of integrated health financing

Several articles discussed the complex system that splits and shares the funding and provision of services between the federal and state governments.4,5,6,7,8,9 The division of roles and responsibilities between levels of government is understood to “undermine cohesive national reform”,4 and “cost and blame shifting” leads to gaps in services5 and budget silos that undermine efficiency.9

The current financing structure reflects a complex and fragmented health care system that struggles to provide effective patient‐centred care;10 patients experience a lack of integration, coordination, and continuity of care between sectors.4,11,12,13 The fee‐for‐service funding model underpinning the Medicare Benefits Schedule (MBS) makes integrated care difficult, particularly for patients with complex chronic disorders and multiple problems who require multidisciplinary, coordinated care.7,9,12

Several models of integrated care have been tried in Australia, but progress toward a national integrated system has been disappointing.9 Medicare Locals (meso‐level organisations) were established by the 2011 National Health Reform to improve the integration of primary care.4,11 They were replaced by Primary Health Networks (PHNs) in 2015,14 but, unsupported by effective policy settings, their influence on the efficiency and effectiveness of medical service provision has been limited.5

The Enhanced Primary Care (EPC) program, introduced in 1999 (since 2004: Chronic Disease Management [CDM]), allowed capped funding for five allied health professional service visits per patient each year.4 Although EPC/CDM programs addressed some allied health service access barriers, the number of funded sessions can be inadequate for meeting the needs of patients or improving health outcomes,15,16 and there are few incentives for providing collaborative care under the fee‐for‐service payment model.4

About 30% of chronic disease in Australia is considered preventable,5 but only 1.8% of health care spending is for preventive interventions.17 An OECD analysis found that primary health care accounted for 17% of Australian health care expenditure in 2019, including 0.2% for prevention; this is lower than the OECD mean (1.0%) and the level in other high income countries (eg, the United Kingdom: 2.7%).18 The fee‐for‐service funding model has been criticised for not providing incentives for health promotion and prevention activities.4,8,12

A key recommendation of the recent MBS Review Task Force was to consider alternative funding models, such as block funding or blended payments, complementing the current fee‐for‐service‐based system and allowing a more integrated, patient‐centred approach and greater emphasis on preventive health care and better management of chronic diseases.14

Access of Aboriginal and Torres Strait Islander people to health services and essential medications

One of the major shortcomings of the Australian universal health care system is that it does not achieve the same health outcomes for Indigenous and non‐Indigenous Australians.4,10,19,20,21 The first Aboriginal Community Controlled Health Organisation (ACCHO) was established in 1971, after a long struggle by Aboriginal and Torres Strait Islander peoples to take control of their health care. ACCHOs directly deliver primary health care services to Indigenous Australians,4,10 often with better performance and outcomes than general practice overall.10 Increased MBS enrolment and rates of health care use were achieved by relaxing enrolment procedures, allowing MBS reimbursement for services provided by nurses and Aboriginal health care workers.4

A number of strategies have aimed to improve the access of Aboriginal and Torres Strait Islander people to essential medications; for example, the Special Pharmaceutical Benefits Scheme Agreement used bulk procurement without co‐payments to improve access to Pharmaceutical Benefits Scheme (PBS) drugs for people attending Aboriginal and Torres Strait Islander health services and ACCHOs.19 The Closing the Gap PBS strategy (2010) was designed to reduce medication co‐payments for all PBS prescription items for Indigenous Australians at risk of or living with chronic medical conditions;21 it improved access to medications, and reduced out‐of‐pocket payments20,21 and hospitalisations.20

Reform proposals for the Pharmaceutical Benefits Scheme (PBS)

Generic drugs are more expensive in Australia than in other countries.22,23,24,25 Measures undertaken to reduce PBS costs26 and “to achieve better value for money from the drugs that are subject to price competition”27 included mandatory 12.5% price reductions and a PBS reform package that established two formularies — the F1 (single brand drugs) and F2 (generic drugs or interchangeable alternatives)22 — with lower prices for F2 drugs and compensation for community pharmacies and wholesalers for their consequent loss of income.22,27

Initial evaluations of these measures yielded mixed results,27 but more recent analyses suggest they have achieved substantial cost savings.24,26,28 Further savings through drug pricing policy may be possible.24,29

The burden of out‐of‐pocket costs

Out‐of‐pocket costs for patients have long been discussed as a key problem of the Australian health care system.30,31,32,33,34,35,36,37,38 In 2018–19, mean personal out‐of‐pocket health‐related costs amounted to about $1649 per person, or 2.6% of mean annual income in Australia.39 Between 2013 and 2019, health‐related out‐of‐pocket costs rose by 24%, outstripping the rise in the consumer price index for this period (11%).40 Out‐of‐pocket costs accounted for 18% of health care expenditure in 2019: slightly lower than the OECD mean (20%), but higher than in countries with similar government‐funded health care systems (the United Kingdom, 16%; New Zealand, 13%; Canada, 15%).18

Sources of out‐of‐pocket costs

The major causes of out‐of‐pocket costs were non‐PBS pharmaceuticals, and dental and medical services;39,41 in the non‐hospital Medicare category, the major contributors were specialists’ services (33.7%), general practitioner services (24.6%), and diagnostic services (12.3%).42

The uncoordinated Australian co‐payment structure does not restrain out‐of‐pocket costs.38 Practices and practitioners are free to set their fees;37,43,44,45 if the federal government sets Medicare fees at low levels (eg, the “Medicare freeze” that ended inflation‐based indexation),43 patients must pay the difference as co‐payments.14,46 The problem is compounded by physician shortages, the high costs of rural practice, and the uneven geographic distribution of general practitioners, which can affect the bulk‐billing behaviour of some practices.32,45,46,47

Some specialists charge patients more than twice the relevant MBS fees,48 and some surgeons more than three times the MBS rate for common procedures.49 Specialists often do not discuss out‐of‐pocket costs with patients in advance, which can result in unexpectedly large costs for the patient.30,36

Impact of out‐of‐pocket costs

Out‐of‐pocket costs can lead patients to forgo or defer health care.30,32,33,34,36,50,51,52,53,54 The Australian Bureau of Statistics 2016–17 Patient Experiences Survey found that 7.6% of people aged 15 years or more (1.3 million people) deferred or did not use specialist, general practice, imaging, or pathology services because of the cost involved.42 People with chronic conditions were more likely to forgo health care because of cost than people in other high income countries.53 Some people skipped appointments or did not use prescribed medication because of cost, reported they could not pay for other living expenses, or drew on their savings or superannuation or sold assets to pay for health care.36,55 Although the absolute level of out‐of‐pocket costs is higher for those on higher incomes,35,56 their burden is greater for people in disadvantaged groups32,43 or with chronic medical conditions.30,32,34,52,53,57 The burden of out‐of‐pocket costs increases with the number of chronic conditions reported,57,58 and is particularly great for people with cancer.59 One study found that the likelihood of spending 10% or more of household income on health care during 2006–2014 was fifteen times as high for people in the lowest income decile as for those in the highest decile.31 People who live outside capital cities, couples with children, people with chronic conditions, and people with private health insurance have higher out‐of‐pocket costs than other people.16,30,32,35,36,37,38,53,57,60

Containing rising out‐of‐pocket costs

Efforts by the Australian government to contain rising out‐of‐pocket costs34 have been criticised. Medicare “safety nets” were introduced in 1984 to provide additional rebates for eligible Australians who incur higher out‐of‐pocket costs for Medicare‐eligible non‐hospital services. However, relatively few people are eligible, and the scheme is poorly targeted5 and does not adequately protect patients from high costs,55,59 and even eligible patients must make large upfront payments for services before claiming the rebate.34,52 The Extended Medicare Safety Net, introduced in 2004, did not achieve its aims, and might motivate providers to change consumer billing practices and increase their fees. Further, it mostly benefits people in wealthier and metropolitan areas, and does not effectively reduce the financial burden on people living with socio‐economic disadvantage.12

The Strengthening Medicare reforms introduced in 2004 and 2005 included incentives for bulk‐billing and reimbursement for all general practice visit costs.61 These reforms had only small and contradictory effects,62 and the reduction in out‐of‐pocket costs achieved was less than the cost to the federal government. People with concession cards appear to be protected better than other people against out‐of‐pocket expenses for general practice services,44 but not against those for specialist services.44,62

The Australian Department of Health and Ageing launched its online medical costs finder tool in December 2019 to allow people to check the costs of common specialist services, including the most recent publicly available data on out‐of‐pocket costs.63

Details of published recommendations and proposals regarding out‐of‐pocket costs for patients are summarised in the Supporting Information, part 3.

Inequity

One of the primary objectives of the universal health care system is equitable access to care.64 Medicare provided a generally “equitable distribution” of access to health care in 2001, but people with higher incomes were more likely to see specialists, those on lower incomes general practitioners.65 A more recent analysis found socio‐economic differences in the probability of general practice visits62,66 and the use of allied health services,14 but the distribution of hospital‐based care was equitable.66 A 2013 study of non‐emergency treatment in public hospitals found that waiting times for people in areas of higher socio‐economic advantage were significantly shorter than for those from disadvantaged areas.64

Inequities in health care access, most marked for people in rural areas and outer suburban areas of major cities,5,8,14,45 can lead to health system inefficiency. For example, people who could be managed in primary care or with limited access to health services are more likely to seek care in emergency departments.67

Gaps in universal health care system coverage for some services (eg, dental and some allied health care) have implications for access.14,68 For example, out‐of‐pocket costs for people with mental health conditions are considerable, and they are more likely to forgo treatment because of cost.53 The cost of dental treatment is largely borne by patients, few being eligible for subsidised dental services, for which waiting times are, in any case, long.69 Moreover, private health insurance for dental services (held by just over one‐half of Australians) covers only 54% of dental care costs.69 Compared with the United Kingdom and Canada, Australians are less likely to visit the dentist in a given year, and people on all income levels are likely to forgo dental treatment, particularly those on low incomes.69

Public subsidies for private health insurance

In response to the problem of younger people opting out of private health insurance, the Australian government encourages private health insurance with financial incentives, tax penalties, and community ratings70,71 (Box 4).

The rationale for private health insurance subsidies was to reduce the costs of publicly funded health care. However, this policy has been criticised for undermining the universality of Medicare.70 Further, attracting people aged 18–30 years is critical for improving the risk pool of private health insurance,72 but rebates, the Medicare levy surcharge, and lifetime health cover do not benefit young people and may therefore no longer be effective for increasing private insurance uptake.71 Some critics even argue that the rebate increases rather than reduces pressure on the public health system.73 Moreover, the opportunity costs to the health system of the private health insurance rebate and subsidies are large, and the money could be more cost‐effectively invested in other programs, such as public hospitals and chronic disease prevention in primary care.4,73,74

Finally, the question of whether private health care should be regarded as a substitute for or a complement to public system services, never satisfactorily explored in Australian policy discussions, is crucial to deciding whether public subsidies for private health insurance are justified.70

Co‐payments and the costs of private health insurance

Limited private health insurance uptake and high attrition are explained mainly by the rising cost of premiums48,70,74 and unexpectedly high out‐of‐pocket costs despite insurance.36,48,74 People also express dissatisfaction with the insurance itself, especially unexpected exclusions and restrictions of coverage.48,49,70 Many people who retain it choose to reduce their cover because of perceptions of limited value,5,74 some concerned that its expense reduces their quality of life.75

A private health insurance “death spiral” has been described: young and healthy people do not purchase or abandon it, leaving private health insurance holders who are typically older and more likely to require health services, leading to greater increases in premiums and consequently further dropouts, which will accelerate its decline unless the levels of private hospital costs and specialist fees are controlled.48

Efficiency and equity

One analysis found that women who gave birth in private hospitals had greater access to obstetric and specialist services and pathology tests, were twice as likely to have caesarean deliveries, and had higher out‐of‐pocket costs than women receiving public hospital care.54 More broadly, lengths of stay are longer for private than public hospitals after adjusting for case complexity and were more likely to offer low value care.48 People with private health insurance have more options for choosing doctors,4,70 shorter waiting times,4,70,72 and access to service options not available to people for whom insurance premiums and gap payments are unaffordable.70,75,76

Other challenges for universal health care in Australia

Other questions discussed in the reviewed literature included the complexity of the medical billing and payment system77 and of implementing changes to Medicare;78 long waiting times for medical care;13,36 low value care and obsolete items in the MBS schedule;12 and public demands for more health care workers.79

Discussion

We found that a range of long standing questions and challenges remain unresolved. The complex divisions in the governance, funding, and provision of health care contribute to its fragmentation in Australia. Reforms have been slow and inadequate for moving toward a more integrated, coordinated, and patient‐centred system. The consensus in the reviewed literature was that traditional fee‐for‐service payment models should be complemented or replaced by alternatives that encourage coordinated care for people with chronic conditions and discourage low value care. The recent evaluation of the Health Care Homes trial reinforces this finding, but also warns of the complexity of delivering reform on a large scale.80

Out‐of‐pocket health care costs are undermining the goal of universal health care in Australia. This is of particular concern for people in regional centres and rural areas, where bulk‐billing rates are lower than in large cities.81 Despite the impact of out‐of‐pocket costs, user fees and out‐of‐pocket costs are not effectively regulated. Measures such as indexation and relaxed regulation of doctors’ fees increase out‐of‐pocket costs, while Medicare safety nets, concession cards, and other measures for reducing their impact are inadequate and poorly targeted. However, inappropriate billing practices and fraud were not identified as major problems in the articles we reviewed, despite the recent media attention they have attracted.82

Despite initiatives undertaken over the past twenty years, programs with the aim of improving health care for Aboriginal and Torres Strait Islander people are still inadequate. Nevertheless, successful improvements and innovations in Indigenous health care could provide useful models for wider reform of Australian health care.

Some generic drugs are more expensive in Australia than in comparable countries, and PBS reform packages were deemed outdated and ineffective for maximising the cost savings generic drugs could achieve. Socio‐economic and ethnic background‐related inequalities in access remain problems, particularly access to dental and mental health care.

Our review also highlighted the continuing lack of policy coherence regarding subsidies to the private health sector without evidence of their providing value for money.

Limitations

Including grey and unpublished literature in our review reduced publication and reporting bias, but excluding articles published before 2000 and studies published after August 2021 were limitations. Title and abstract screening was undertaken by a single author. As we focused on the general Australian population, some specific groups were excluded, including asylum seekers, whose access to health care services that recognises their cultural needs (including the availability of interpreters and bilingual health care providers) is limited by their visa conditions.83,84,85,86,87,88 Most of the period covered by our review preceded the COVID‐19 pandemic in Australia, and it consequently does not reflect its acute and longer term effects on health care needs. The explicitly financial focus of our review meant that some other important factors were not examined, particularly health professional supply, and stress and burnout among health workers, and the implications of climate change and extreme weather events for health care. Similarly, we did not address the “causes of the causes” of ill‐health: structural and socio‐economic inequities,89 the commercial determinants of health, and the consumptagenic environment in which we live, driving overconsumption that undermines human and planetary health.90

Conclusions

We found that reforms of the universal health care system over the past twenty years have been piecemeal and uncoordinated, inadequate for alleviating its systemic problems. Further, the scope of the new Strengthening Medicare taskforce inadequately covers important challenges, not least because it is primarily focused on general practice.2 It is unclear whether reforms within the comfort zones of current stakeholders (eg, commitment only to voluntary patient registration in general practice by Strengthening Medicare) can deliver the degree of structural change required to safeguard and strengthen universal health care in Australia. Effective reform that simultaneously reduces fragmentation and improves whole system integration requires that the dominance of fee‐for‐service payments in the health system be replaced by carefully designed block‐funding, capitation, and outcomes‐based funding. The Australian government must develop clear policy goals and mechanisms for regulating fees and controlling out‐of‐pocket costs, re‐examine public subsidies for private health care, and confirm the centrality of equitable access to genuinely universal health care. The current crisis in primary care requires a fundamental readjustment of supply, remuneration, and professional status between general practitioners and other specialties that goes well beyond financial questions. This will require deep engagement in good faith from doctors and governments alike. Effective, systemic, and comprehensive reforms of the Australian health system were overdue before the COVID‐19 pandemic; they are now essential if universal health care for all Australians is to be a reality rather than rhetoric.

Box 1 – Simplified schematic depiction of health care financing in Australia

ABF = activity‐based funding; GPP = general purpose payments; GST = goods and services tax; MBS = Medicare Benefits Schedule; OOP = out‐of‐pocket expenses; PBS = Pharmaceutical Benefits Scheme; PHI = private health insurance; SPP = specific purpose payments.

Box 2 – Selection of publications on the Australian health care system for inclusion in our review

* Analysis & Policy Observatory, the Australian Indigenous HealthInfoNet, the Australian Public Affairs Information Service, Google, Google Scholar, and the Organisation for Economic Co‐operation and Development (OECD) websites.

Box 4 – Australian government surcharges and incentives related to private health insurance

|

Surcharge/incentive |

Description |

Comments from the literature reviewed |

|||||||||||||

|

|

|||||||||||||||

|

Private health insurance rebate |

Privately insured people can receive rebates from the Australian government. |

Criticisms

Positive comments

|

|||||||||||||

|

Age‐based discounts |

Insurers can provide young adults (18–29 years) discounts of up to 10% since 1 April 2019.71 |

|

|||||||||||||

|

Lifetime health cover |

Penalises young people aged 31 years or more who do not have private hospital insurance by increasing their premiums71 |

Positive:

|

|||||||||||||

|

Means‐tested Medicare levy surcharge |

A levy for people with incomes beyond a threshold and do not have private hospital cover71 |

|

|||||||||||||

|

|

|||||||||||||||

|

|

|||||||||||||||

Provenance: Not commissioned; externally peer reviewed.

- Mary Rose Angeles1

- Paul Crosland2

- Martin Hensher3

- 1 Deakin University, Melbourne, VIC

- 2 Brain and Mind Centre, the University of Sydney, Sydney, NSW

- 3 Menzies Institute for Medical Research, the University of Tasmania, Hobart, TAS

Open access

Open access publishing facilitated by University of Tasmania, as part of the Wiley ‐ University of Tasmania agreement via the Council of Australian University Librarians.

No relevant disclosures.

- 1. Schneider EC, Shah A, Doty MM, et al. Mirror, Mirror 2021: reflecting poorly: health care in the US compared to other high‐income countries. The Commonwealth Fund, 4 Aug 2021. https://www.commonwealthfund.org/publications/fund‐reports/2021/aug/mirror‐mirror‐2021‐reflecting‐poorly (viewed June 2022).

- 2. Australian Department of Health and Aged Care. Strengthening Medicare taskforce. Updated 14 Nov 2022. https://www.health.gov.au/committees‐and‐groups/strengthening‐medicare‐taskforce (viewed Nov 2022).

- 3. Biggs A. Medicare: background brief [Parliamentary Library]. Updated 29 Oct 2004. https://parlinfo.aph.gov.au/parlInfo/download/library/prspub/8823863/upload_binary/8823863.pdf;fileType=application%2Fpdf#search=%22background%20brief%22 (viewed Aug 2022).

- 4. McPake B, Mahal A. Addressing the needs of an aging population in the health system: the Australian case. Health Syst Reform 2017; 3: 236‐247.

- 5. Calder R, Dunkin R, Rochford C, Nichols T. Australian health services: too complex to navigate: a review of the national reviews of Australia's health service arrangements [policy paper]. 28 Feb 2019. https://apo.org.au/node/223011 (viewed Aug 2021).

- 6. Blecher GE, Blashki GA, Judkins S. Crisis as opportunity: how COVID‐19 can reshape the Australian health system. Med J Aust 2020; 213: 196‐198. https://www.mja.com.au/journal/2020/213/5/crisis‐opportunity‐how‐covid‐19‐can‐reshape‐australian‐health‐system

- 7. Hayes P, Lynch A, Stiffe J. Moving into the “patient‐centred medical home”: reforming Australian general practice. Educ Prim Care 2016; 27: 413‐415.

- 8. Roberts R. Vale Bob Hawke: what impact has Medicare had on rural Australia? Aust J Rural Health 2019; 27: 194‐195.

- 9. Productivity Commission. Integrated care, shifting the dial: 5 year productivity review [supporting paper no. 5]. 5 Aug 2017. https://www.pc.gov.au/inquiries/completed/productivity‐review/report/productivity‐review‐supporting5.pdf (viewed Aug 2021).

- 10. Nolan‐Isles D, Macniven R, Hunter K, et al. Enablers and barriers to accessing healthcare services for Aboriginal people in New South Wales, Australia. Int J Environ Res Public Health 2021; 18: 3014.

- 11. Robinson S, Varhol R, Ramamurthy V, et al. The Australian primary healthcare experiment: a national survey of Medicare Locals. BMJ Open 2015; 5: e007191.

- 12. Medicare Benefits Schedule Review Taskforce. An MBS for the 21st century: recommendations, learnings and ideas for the future. Medicare Benefits Schedule Review Taskforce final report to the Minister for Health. 14 Dec 2020. https://www.health.gov.au/resources/publications/medicare‐benefits‐schedule‐review‐taskforce‐final‐report (viewed Aug 2021).

- 13. Dixit SK, Sambasivan M. A review of the Australian healthcare system: a policy perspective. SAGE Open Med 2018; 6: 2050312118769211.

- 14. Fisher M, Baum F, Kay A, Friel S. Are changes in Australian national primary healthcare policy likely to promote or impede equity of access? A narrative review. Aust J Prim Health 2017; 23: 209‐215.

- 15. Haines TP, Foster MM, Cornwell P, et al. Impact of enhanced primary care on equitable access to and economic efficiency of allied health services: a qualitative investigation. Aust Health Rev 2010; 34: 30‐35.

- 16. Callander E, Larkins S, Corscadden L. Variations in out‐of‐pocket costs for primary care services across Australia: a regional analysis. Aust J Prim Health 2017; 23: 379‐385.

- 17. Jackson H, Shiell A. Preventive health: how much does Australia spend and is it enough? Canberra: Foundation for Alcohol Research and Education, 2017. https://fare.org.au/wp‐content/uploads/Preventive‐health‐How‐much‐does‐Australia‐spend‐and‐is‐it‐enough_FINAL.pdf (viewed Aug 2021).

- 18. Organisation for Economic Co‐operation and Development. Health at a glance 2021: OECD indicators [cited: figures 7.17 and 7.9]. 9 Nov 2021. https://doi.org/10.1787/ae3016b9‐en (viewed Aug 2021).

- 19. Kelaher M, Dunt D, Taylor‐Thomson D, et al. Improving access to medicines among clients of remote area Aboriginal and Torres Strait Islander Health Services. Aust N Z J Public Health 2006; 30: 177‐183.

- 20. Trivedi AN, Bailie R, Bailie J, et al. Hospitalizations for chronic conditions among Indigenous Australians after medication copayment reductions: the closing the gap copayment incentive. J Gen Intern Med 2017; 32: 501‐507.

- 21. Trivedi AN, Kelaher M. Copayment incentive increased medication use and reduced spending among Indigenous Australians after 2010. Health Aff (Millwood) 2020; 39: 289‐296.

- 22. Bulfone L. High prices for generics in Australia: more competition might help. Aust Health Rev 2009; 33: 200‐214.

- 23. Mansfield SJ. Generic drug prices and policy in Australia: room for improvement? A comparative analysis with England. Aust Health Rev 2014; 38: 6‐15.

- 24. Duckett S, Banerjee P. Cutting a better drug deal [Grattan Institute report no. 2017‐03], 5 Mar 2017. https://grattan.edu.au/report/cutting‐a‐better‐drug‐deal (viewed Aug 2021).

- 25. Medbelle. 2019 Medicine price index. Undated. https://www.medbelle.com/medicine‐price‐index‐usa (viewed Aug 2021).

- 26. GlaxoSmithKline Australia, ViiV Healthcare. The Pharmaceutical Benefits Scheme in Australia: an explainer on system components. Feb 2018. https://au.gsk.com/media/6259/gsk‐viiv‐the‐pbs‐in‐australia‐feb‐2018.pdf (viewed Aug 2021).

- 27. Australian Department of Health and Ageing. The impact of PBS reform: report to Parliament on the National Health Amendment (Pharmaceutical Benefits Scheme) Act 2007. 2010. https://apo.org.au/sites/default/files/resource‐files/2010‐02/apo‐nid20402.pdf (viewed Aug 2021).

- 28. Spinks J, Chen G, Donovan L. Does generic entry lower the prices paid for pharmaceuticals in Australia? A comparison before and after the introduction of the mandatory price‐reduction policy. Aust Health Rev 2013; 37: 675‐681.

- 29. Karnon J, Edney L, Sorich M. Costs of paying higher prices for equivalent effects on the Pharmaceutical Benefits Scheme. Aust Health Rev 2017; 41: 1‐6.

- 30. Bygrave A, Whittaker K, Paul C, et al. Australian experiences of out‐of‐pocket costs and financial burden following a cancer diagnosis: a systematic review. Int J Environ Res Public Health 2021; 18: 2422.

- 31. Callander EJ, Fox H, Lindsay D. Out‐of‐pocket healthcare expenditure in Australia: trends, inequalities and the impact on household living standards in a high‐income country with a universal health care system. Health Econ Rev 2019; 9: 10.

- 32. Duckett S, Breadon P. Out‐of‐pocket costs: hitting the most vulnerable hardest. Grattan Institute submission to the Senate Standing Committee on Community Affairs Inquiry into the out‐of‐pocket costs in Australian healthcare. May 2014. https://grattan.edu.au/wp‐content/uploads/2014/07/Grattan_Institute_submission_‐_inquiry_on_out‐of‐pocket_costs_‐_FINAL.pdf (viewed Aug 2021).

- 33. Kemp A, Preen DB, Glover J, et al. How much do we spend on prescription medicines?: out‐of‐pocket costs for patients in Australia and other OECD countries. Aust Health Rev 2011; 35: 341‐349.

- 34. Russell L, Doggett J. A road map for tackling out‐of‐pocket health care costs. Analysis & Policy Observatory, 11 Feb 2019. https://apo.org.au/node/219221 (viewed Aug 2021).

- 35. Yusuf F, Leeder S. Recent estimates of the out‐of‐pocket expenditure on health care in Australia. Aust Health Rev 2020; 44: 340‐346.

- 36. Consumers Health Forum of Australia. Out of pocket pain: research report. 5 Apr 2018. https://chf.org.au/publications/out‐pocket‐pain (viewed Aug 2021).

- 37. Young AF, Dobson AJ. The decline in bulk‐billing and increase in out‐of‐pocket costs for general practice consultations in rural areas of Australia, 1995–2001. Med J Aust 2003; 178: 122‐126. https://www.mja.com.au/journal/2003/178/3/decline‐bulk‐billing‐and‐increase‐out‐pocket‐costs‐general‐practice

- 38. Yusuf F, Leeder SR. Can't escape it: the out‐of‐pocket cost of health care in Australia. Med J Aust 2013; 199: 475‐478. https://www.mja.com.au/journal/2013/199/7/cant‐escape‐it‐out‐pocket‐cost‐health‐care‐australia

- 39. Australian Institute of Health and Welfare. Health expenditure Australia 2018–19 (Cat. no. HWE 80; Health and welfare expenditure series no. 66). Canberra: AIHW, 2020. https://www.aihw.gov.au/getmedia/a5cfb53c‐a22f‐407b‐8c6f‐3820544cb900/aihw‐hwe‐80.pdf.aspx?inline=true (viewed Aug 2021).

- 40. Richardson D. Health costs outpace inflation [briefing note]. The Australia Institute, 2 May 2019. https://australiainstitute.org.au/report/health‐costs‐outpace‐inflation (viewed Aug 2021).

- 41. Johnson C. Health spending figures show non‐PBS medications driving out‐of‐pockets [news]. Australian Medicine 2019; 31 (18): 10.

- 42. Australian Institute of Health and Welfare. Patients’ out‐of‐pocket spending on Medicare services 2016–17 (Cat. no. HPF 35). 16 Aug 2018. https://www.aihw.gov.au/reports/health‐welfare‐expenditure/patient‐out‐pocket‐spending‐medicare‐2016‐17/contents/summary (viewed Aug 2021).

- 43. Elkins RK, Schurer S. Introducing a GP copayment in Australia: who would carry the cost burden? Health Policy 2017; 121: 543‐552.

- 44. Jones G, Savage E, Van Gool K. The distribution of household health expenditures in Australia. Economic Record 2008; 84 (Suppl 1): S99‐S114.

- 45. Kenny A, Duckett S. A question of place: medical power in rural Australia. Soc Sci Med 2004; 58: 1059‐1073.

- 46. Rollins A. Fees gap widens as costs rise but rebates don't [news]. Australian Medicine 2016; 28 (10): 8‐9.

- 47. Harrison C, Bayram C, Miller GC, Britt HC. The cost of freezing general practice. Med J Aust 2015; 202: 313‐316. https://www.mja.com.au/journal/2015/202/6/cost‐freezing‐general‐practice

- 48. Duckett S, Nemet K. Saving private health. 1. Reining in hospital costs and specialist bills. Grattan Institute, Nov 2019. https://grattan.edu.au/wp‐content/uploads/2019/11/925‐Saving‐private‐health‐1.pdf (viewed Aug 2021).

- 49. Dobrosak C, Dugdale P. Issues for reregulation of private hospital insurance in Australia. Aust Health Rev 2021; 45: 290‐296.

- 50. Hynd A, Roughead EE, Preen DB, et al. The impact of co‐payment increases on dispensings of government‐subsidised medicines in Australia. Pharmacoepidemiology Drug Saf 2008; 17: 1091‐1099.

- 51. Sweeny K. The impact of copayments and safety nets on PBS expenditure. Aust Health Rev 2009; 33: 215‐230.

- 52. Walkom EJ, Loxton D, Robertson J. Costs of medicines and health care: a concern for Australian women across the ages. BMC Health Serv Res 2013; 13: 484.

- 53. Callander EJ, Corscadden L, Levesque JF. Out‐of‐pocket healthcare expenditure and chronic disease: do Australians forgo care because of the cost? Aust J Prim Health 2017; 23: 15‐22.

- 54. Callander EJ, Topp S, Fox H, Corscadden L. Out‐of‐pocket expenditure on health care by Australian mothers: lessons for maternal universal health coverage from a long‐established system. Birth 2020; 47: 49‐56.

- 55. Carpenter A, Islam MM, Yen L, McRae I. Affordability of out‐of‐pocket health care expenses among older Australians. Health Policy 2015; 119: 907‐914.

- 56. Hua X, Erreygers G, Chalmers J, et al. Using administrative data to look at changes in the level and distribution of out‐of‐pocket medical expenditure: an example using Medicare data from Australia. Health Policy 2017; 121: 426‐433.

- 57. McRae I, Yen L, Jeon YH, et al. Multimorbidity is associated with higher out‐of‐pocket spending: a study of older Australians with multiple chronic conditions. Aust J Prim Health 2013; 19: 144‐149.

- 58. Islam MM, Yen L, Valderas JM, McRae IS. Out‐of‐pocket expenditure by Australian seniors with chronic disease: the effect of specific diseases and morbidity clusters. BMC Public Health 2014; 14: 1008.

- 59. Gordon LG, Elliott TM, Olsen CM, et al ; QSkin Study. Patient out‐of‐pocket medical expenses over 2 years among Queenslanders with and without a major cancer. Aust J Prim Health 2018; 24: 530‐536.

- 60. Slavova‐Azmanova NS, Newton JC, Johnson CE, et al. A cross‐sectional analysis of out‐of‐pocket expenses for people living with a cancer in rural and outer metropolitan Western Australia. Aust Health Rev 2021; 45: 148‐156.

- 61. Wong CY, Greene J, Dolja‐Gore X, van Gool K. The rise and fall in out‐of‐pocket costs in Australia: an analysis of the Strengthening Medicare reforms. Health Econ 2017; 26: 962‐979.

- 62. Pulok MH, Van Gool K, Hall J. Inequity in physician visits: the case of the unregulated fee market in Australia. Soc Sci Med 2020; 255: 113004.

- 63. Australian Department of Health and Ageing. Medical costs finder. Updated 1 Sept 2021. https://www.health.gov.au/resources/apps‐and‐tools/medical‐costs‐finder (viewed June 2022).

- 64. Johar M, Jones G, Keane MP, et al. Discrimination in a universal health system: explaining socioeconomic waiting time gaps. J Health Econ 2013; 32: 181‐194.

- 65. Van Doorslaer E, Clarke P, Savage E, Hall J. Horizontal inequities in Australia's mixed public/private health care system. Health Policy 2008; 86: 97‐108.

- 66. Pulok MH, Van Gool K, Hall J. Horizontal inequity in the utilisation of healthcare services in Australia. Health Policy 2020; 124: 1263‐1271.

- 67. Pak A, Gannon B. Do access, quality and cost of general practice affect emergency department use? Health Policy 2021; 125: 504‐511.

- 68. Pearce‐Brown CL, Grealish L, McRae IS, et al. A local study of costs for private allied health in Australian primary health care: variability and policy implications. Aust J Prim Health 2011; 17: 131‐134.

- 69. Duckett S, Cowgill M, Swerissen H. Filling the gap: a universal dental care scheme for Australia. Grattan Institute, 17 Mar 2019. https://apo.org.au/node/225591 (viewed Aug 2021).

- 70. Duckett S, Nemet K. The history and purposes of private health insurance. Grattan Institute, July 2019. https://grattan.edu.au/wp‐content/uploads/2019/07/918‐The‐history‐and‐purposes‐of‐private‐health‐insurance.pdf (viewed Aug 2021).

- 71. Zhang Y. Private hospital insurance premiums should vary by age. InSight+, 5 Oct 2020. https://insightplus.mja.com.au/2020/39/private‐hospital‐insurance‐premiums‐should‐vary‐by‐age (viewed Aug 2021).

- 72. Tam L, Tyquin E, Mehta A, Larkin I. Determinants of attitude and intention towards private health insurance: a comparison of insured and uninsured young adults in Australia. BMC Health Serv Res 2021; 21: 246.

- 73. Eckermann S, Sheridan L, Ivers R. Which direction should Australian health system reform be heading? Aust N Z J Public Health 2016; 40: 7‐9.

- 74. Zhang Y, Prakash K. What influences whether we buy private hospital insurance? InSight+, 7 June 2021. https://insightplus.mja.com.au/2021/20/why‐do‐australians‐buy‐private‐hospital‐insurance (viewed Aug 2021).

- 75. Jeon YH, Black A, Govett J, et al. Private health insurance and quality of life: perspectives of older Australians with multiple chronic conditions. Aust J Prim Health 2012; 18: 212‐219.

- 76. Robertson‐Preidler J, Anstey M, Biller‐Andorno N, Norrish A. Approaches to appropriate care delivery from a policy perspective: a case study of Australia, England and Switzerland. Health Policy 2017; 121: 770‐777.

- 77. Faux M, Wardle J, Adams J. Medicare billing, law and practice: complex, incomprehensible and beginning to unravel. J Law Med 2019; 27: 66‐93.

- 78. Australian Medical Association. Government in danger of history repeating with Medicare rebate changes [media release]. 6 June 2021. https://www.ama.com.au/media/government‐danger‐history‐repeating‐medicare‐rebate‐changes (viewed Aug 2021)

- 79. Ellis LA, Pomare C, Gillespie JA, et al. Changes in public perceptions and experiences of the Australian health‐care system: a decade of change. Health Expect 2021; 24: 95‐110.

- 80. Pearse J, Mazevska D, McElduff P, et al. Evaluation of the Health Care Homes trial. Volume 1. Summary report. Australian Department of Health, 29 July 2022. https://www.health.gov.au/resources/publications/evaluation‐of‐the‐health‐care‐homes‐trial‐final‐evaluation‐report‐2022 (viewed Aug 2022).

- 81. Australian Department of Health and Aged Care. Medicare annual statistics: rolling 12 months (2009–10 to 2021–22). 14 Nov 2022. https://www.health.gov.au/resources/publications/medicare‐annual‐statistics‐rolling‐12‐months‐2009‐10‐to‐2021‐22 (viewed Nov 2022).

- 82. Farmer J. Medicare compliance: seeking transparency and fairness. Insight+, 7 Nov 2022. https://insightplus.mja.com.au/2022/43/medicare‐compliance‐seeking‐transparency‐and‐fairness (viewed Jan 2023).

- 83. Correa‐Velez I, Gifford SM, Bice SJ. Australian health policy on access to medical care for refugees and asylum seekers. Aust New Zealand Health Policy 2005; 2: 23.

- 84. Johnston V. Australian asylum policies: have they violated the right to health of asylum seekers? Aust N Z J Public Health 2009; 33: 40‐46.

- 85. Nkhoma G, Lim CX, Kennedy GA, Stupans I. Reducing health inequities for asylum seekers with chronic non‐communicable diseases: Australian context. Aust J Prim Health 2021; 27: 130‐135.

- 86. Spike EA, Smith MM, Harris MF. Access to primary health care services by community‐based asylum seekers. Med J Aust 2011; 195: 188‐191. https://www.mja.com.au/journal/2011/195/4/access‐primary‐health‐care‐services‐community‐based‐asylum‐seekers

- 87. Ziersch A, Freeman T, Javanparast S, et al. Regional primary health care organisations and migrant and refugee health: the importance of prioritisation, funding, collaboration and engagement. Aust N Z J Public Health 2020; 44: 152‐159.

- 88. Corbett EJM, Gunasekera H, Maycock A, Isaacs D. Australia's treatment of refugee and asylum seeker children: the views of Australian paediatricians. Med J Aust 2014; 201: 393‐398. https://www.mja.com.au/journal/2014/201/7/australias‐treatment‐refugee‐and‐asylum‐seeker‐children‐views‐australian

- 89. Marmot M. The health gap: the challenge of an unequal world. London: Bloomsbury Publishing, 2015.

- 90. Friel S. Climate change and the people's health: the need to exit the consumptagenic system. Lancet 2020; 395: 666‐668.

Abstract

Objectives: To identify the financing and policy challenges for Medicare and universal health care in Australia, as well as opportunities for whole‐of‐system strengthening.

Study design: Review of publications on Medicare, the Pharmaceutical Benefits Scheme, and the universal health care system in Australia published 1 January 2000 – 14 August 2021 that reported quantitative or qualitative research or data analyses, and of opinion articles, debates, commentaries, editorials, perspectives, and news reports on the Australian health care system published 1 January 2015 – 14 August 2021. Program‐, intervention‐ or provider‐specific articles, and publications regarding groups not fully covered by Medicare (eg, asylum seekers, prisoners) were excluded.

Data sources: MEDLINE Complete, the Health Policy Reference Centre, and Global Health databases (all via EBSCO); the Analysis & Policy Observatory, the Australian Indigenous HealthInfoNet, the Australian Public Affairs Information Service, Google, Google Scholar, and the Organisation for Economic Co‐operation and Development (OECD) websites.

Results: The problems covered by the 76 articles included in our review could be grouped under seven major themes: fragmentation of health care and lack of integrated health financing, access of Aboriginal and Torres Strait Islander people to health services and essential medications, reform proposals for the Pharmaceutical Benefits Scheme, the burden of out‐of‐pocket costs, inequity, public subsidies for private health insurance, and other challenges for the Australian universal health care system.

Conclusions: A number of challenges threaten the sustainability and equity of the universal health care system in Australia. As the piecemeal reforms of the past twenty years have been inadequate for meeting these challenges, more effective, coordinated approaches are needed to improve and secure the universality of public health care in Australia.